Short Ratio Put Spread

Description

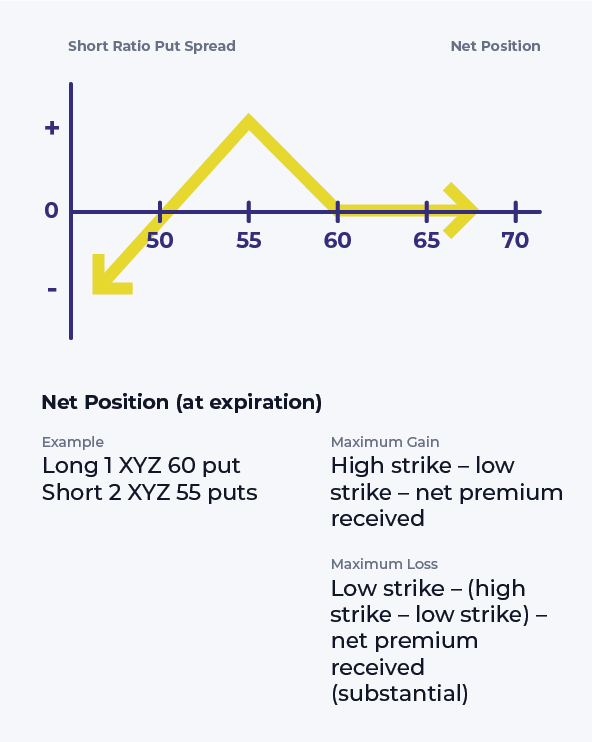

The short ratio put spread involves buying one put (generally at the money) and selling two puts of the same expiration but with a lower strike. This strategy is the combination of a bear put spread and a naked put, where the strike of the naked put is equal to the lower strike of the bear put spread.

Outlook

The investor is ideally hoping for a slow rally up to the strike where they have sold two calls or a sharp fall in implied volatility during the life of the options.

Summary

This strategy can profit from a slight rise, a steady stock price or a falling implied volatility. The actual behavior of the strategy depends largely on the Delta, Theta, and Vega of the combined position as well as whether a debit is paid or a credit received when initiating the position.

Ready to apply what you've learned?

Trade with the Lightspeed advantage and open an account today

Content Licensed from the Options Industry Council. All Rights Reserved. OIC or its affiliates shall not be responsible for content contained on Company’s Website, or other Company Materials not provided by OIC.

Content licensed from the Options Industry Council is intended to educate investors about U.S. exchange-listed options issued by The Options Clearing Corporation, and shall not be construed as furnishing investment advice or being a recommendation, solicitation or offer to buy or sell ant option or any other security. Options involve risk and are not suitable for all investors.