Long Call

Description

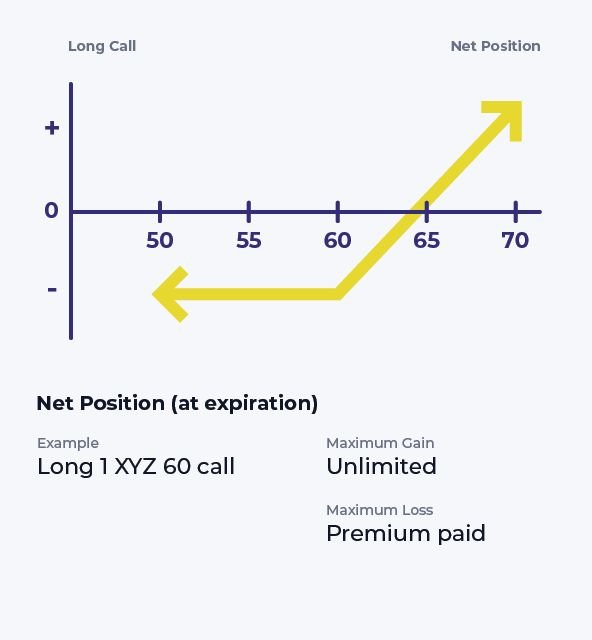

A long call strategy typically doesn’t appreciate a 1-to-1 ratio with the stock, but pricing models often give us a reasonable estimate about how a $1 stock price change might affect the call’s value, assuming other factors remain the same. What’s more, the percentage gains relative to the premium can be significant if the forecast is on target.

The call buyer who plans to resell the option at a profit is looking for suitable opportunities to close the position out early: usually a rally and/or a sharp increase in volatility. Some investors set price targets or re-evaluation dates; others ‘play it by ear.’ Either way, timing is everything for this strategy, because all values must be realized before the option expires. Being right about an anticipated rally does no good if it occurs after expiration.

Ready to apply what you've learned?

Trade with the Lightspeed advantage and open an account today

Content Licensed from the Options Industry Council. All Rights Reserved. OIC or its affiliates shall not be responsible for content contained on Company’s Website, or other Company Materials not provided by OIC.

Content licensed from the Options Industry Council is intended to educate investors about U.S. exchange-listed options issued by The Options Clearing Corporation, and shall not be construed as furnishing investment advice or being a recommendation, solicitation or offer to buy or sell ant option or any other security. Options involve risk and are not suitable for all investors.