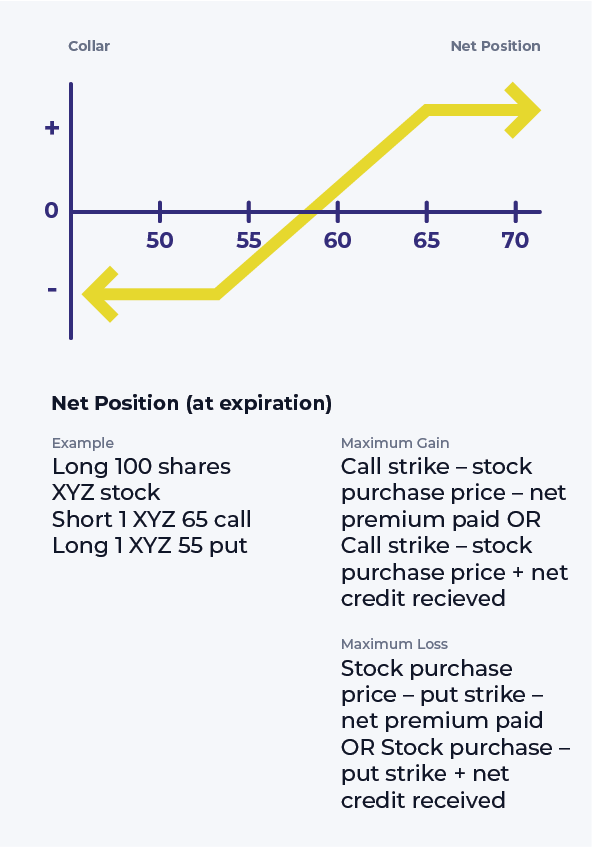

Collar (Protective Collar)

Description

An investor writes a call option and buys a put option with the same expiration as a means to hedge a long position in the underlying stock. This strategy combines two other hedging strategies: protective puts and covered call writing.

Usually, the investor will select a call strike above and a long put strike below the starting stock price. There is latitude, but the strike choices will affect the cost of the hedge as well as the protection it provides. These strikes are referred to as the ‘floor’ and the ‘ceiling’ of the position, and the stock is ‘collared’ between the two strikes.

The put strike establishes a minimum exit price, should the investor need to liquidate in a downturn.

The call strike sets an upper limit on stock gains. The investor should be prepared to relinquish the shares if the stock rallies above the call strike.

In return for accepting a cap on the stock’s upside potential, the investor receives a minimum price where the stock can be sold during the life of the collar.

Outlook

For the term of the option strategy, the investor is looking for a slight rise in the stock price but is worried about a decline.

Ready to apply what you've learned?

Trade with the Lightspeed advantage and open an account today

Content Licensed from the Options Industry Council. All Rights Reserved. OIC or its affiliates shall not be responsible for content contained on Company’s Website, or other Company Materials not provided by OIC.

Content licensed from the Options Industry Council is intended to educate investors about U.S. exchange-listed options issued by The Options Clearing Corporation, and shall not be construed as furnishing investment advice or being a recommendation, solicitation or offer to buy or sell ant option or any other security. Options involve risk and are not suitable for all investors.