Long Call Calendar

Description

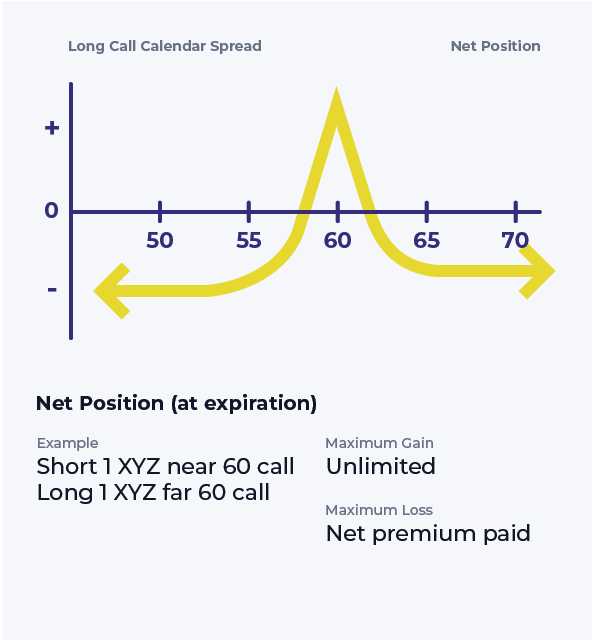

Short one call option and long a second call option with a more distant expiration is an example of a long call calendar spread. The strategy most commonly involves calls with the same strike (horizontal spread), but can also be done with different strikes (diagonal spread).

Outlook

Looking for either a steady to slightly declining stock price during the life of the near-term option and then a move higher during the life of the far-term option, or a sharp move upward in implied volatility.

Summary

This strategy combines a longer-term bullish outlook with a near-term neutral/bearish outlook. If the underlying stock remains steady or declines during the life of the near-term option, that option will expire worthless and leave the investor owning the longer-term option free and clear. If both options have the same strike price, the strategy will always require paying a premium to initiate the position.

Ready to apply what you've learned?

Trade with the Lightspeed advantage and open an account today

Content Licensed from the Options Industry Council. All Rights Reserved. OIC or its affiliates shall not be responsible for content contained on Company’s Website, or other Company Materials not provided by OIC.

Content licensed from the Options Industry Council is intended to educate investors about U.S. exchange-listed options issued by The Options Clearing Corporation, and shall not be construed as furnishing investment advice or being a recommendation, solicitation or offer to buy or sell ant option or any other security. Options involve risk and are not suitable for all investors.